| Email: info@psq.co.za Phone: 021 557 2491

|

|

|

|

Newsletter |

Make or Buy? What About Transfer Price?

It Depends.

By Hank “It Depends” Barr, CPIM-F

I really enjoy talking about prices and costs. It's fascinating to see how one's perspective makes things change. For instance, what does a pound of salmon cost when it's caught off the back of my boat in Puget Sound? My wife, a retired accounting supervisor, thinks it's very expensive and I think it's relatively free. As far as I’m concerned, catching an occasional salmon is just incidental to recreation on the water. I know for sure that when I don’t catch a salmon, I haven’t avoided any boat ownership costs! She will spend a lot of time and gas to shop for a bargain that by my accounting isn’t a bargain at all. We sometimes have very different ways of thinking about and recognizing or allocating costs and some vigorous discussions about them.

Transfer

prices (often internal cost roll ups plus profit) can be very

arbitrary. It's no wonder many organizations think that they can buy

cheaper on the outside than making from the inside. The key is

recognizing that this is a transfer, not a sale nor a purchase. Profit

and contribution to overhead should ideally only come from sales to the

ultimate consumer, or at the very least from a sale to the next

different business member of the supply chain. In fact, allowing

transfer prices at anything above cost of materials will reward and

encourage very expensive pricing. It gives the impression that part of

the organization is generating profits by transferring things to

internal customers who usually don't have a choice of suppliers at

prices that effectively conceal (because of absorption or allocation)

prior expensive decisions.

Traditional, full absorption costing in accordance with GAAP insures

that all costs are assigned to products or services. However the amount

and timing of costs, incurrence or recognition, is dependent on policy

(usually government or management) that changes from time to time and

circumstance to circumstance. As an example, I bought some office

equipment a while back, which I could have capitalized and allocated

its cost over several years or even assigned portions of the cost to

the projects I worked on while using it. However, I chose (in

accordance with IRS guidelines for that tax year) to immediately

expense it. This was an arbitrary management decision, which meant that

for that year, I incurred or recognized more expense than the following

year even though all other activities were relatively constant.

Does that really mean that my services were more costly the first year

than subsequent years? Yes, for tax reporting purposes, but not for

other purposes.

For

many companies, their accounting staff estimates the activities and

events which are expected to happen and the costs (amortized fixed

costs and variable costs) they expect to incur. Next they divide the

expected costs by the expected activities to develop an average cost

per activity. Then they allow (sometimes encourage) people to think

that those costs are somehow incurred (or driven by) those activities

every single time anything occurs; by implication, these costs are

avoided when activities do not occur. Let's examine these

assumptions with an example. Say your company pays your purchasing

agent or shop scheduler $52,000/yr and on average each week they

accomplish 100 transactions for an average transaction cost of

$10. Does that mean that their transaction or activity caused the

incurrence of $10 cost? No! Can you save money by not accomplishing the

transaction or by not doing the activity? Not likely, except for the

materials! So, why did you incur the cost? The real answer is because

people are on the payroll and will generally get paid the same in fast

times, slow times, vacation times and sick times. Payroll is a

relatively fixed expense, which means that the incremental cost or

marginal cost of one more or one less transaction or activity (except

for materials and possibly commissions) is zero.

By the way, what does an incremental cash flow cost of zero do to traditional EOQ or lot size calculations, if you use zero instead of average, fully absorbed cost? Since the change would be zero (S=0), the EOQ formula would reduce to the square root of zero. Then, what about the transfer price for items? Should your department or anybody’s department really have to absorb the transferred consequences of an upstream arbitrary decision on overhead costs? No, do transfers at prime material cost.

A more important measurement of an activity’s cost is its impact on throughput (sales revenue - totally variable costs). Any interruption in production at a bottleneck or revenue pacesetter is very expensive in terms of cash flow. More activity at a non-bottleneck work center usually only affects total costs and cash flow by consuming additional materials. If at the non-bottleneck you do more work, you’ll incur additional material cost, but not much else. Therefore, if you sell something from this additional effort for more than the cost of materials, you will make a positive contribution to overhead and profit.

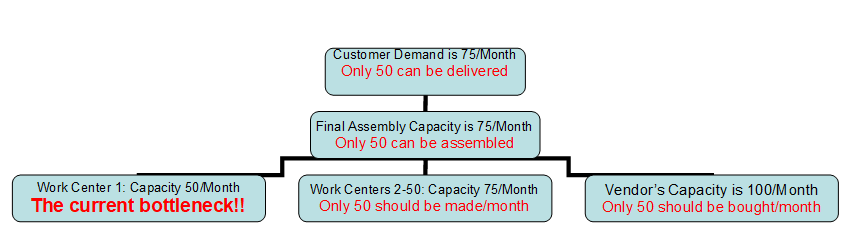

To help everybody in your organization really understand what's happening, map your process flows or value streams so you will know where your bottleneck is for your current product mix. Ask your accounting department to do a little research to show how much total costs actually vary when volumes change, except for materials. You will almost surely find that for the vast majority of time periods, expenses or costs were fixed in the design stage of the product and business. With very few exceptions, the only business expense that fluctuates with production volume is the amount of materials consumed.

To illustrate: An organization has an internal constraint which will not be solved for some time. Work center 1 only has capacity for 50 per month and because of horizontal and vertical dependency, the whole organization and the supply chain is therefore constrained to 50 per month. Fortunately for this business (though not for consumers), economic and political barriers to entry keep its competitors from rushing in to seize upon this unsatisfied demand opportunity. Such barriers won’t last forever! Cost accounting has determined that the overhead at all departments is $140/hour. One unit is sold approximately every day, generating $6,000,000 in profit.

Now consider the following “opportunity” to sell a component product to a customer for $300. You can make the product for $100 in materials using 3 hours of labor and you don’t need to use the constrained (bottleneck) resource to produce it. Or, you can outsource it for a mere $200. What should you do?

Since 3 hours of labor X $140/hr + $100 in materials = $520 of cost compared to the $300 of sales revenue which leads to a loss of $220, traditional cost accounting would say it’s too expensive to make, so “Buy it”! However, that’s not the right decision because if you buy it those are real dollars going out the door and those pesky, relatively fixed, period costs won’t change.

You should “Make it”, since the totally variable cost of materials is only $100 and the sales price is $300 for a positive cash flow and contribution to profit of $200.

Scenario: Cost accounting has determined overhead at all departments to be $140/hour. One end item gets sold every day, generating $6,000,000 in profit.

Now consider the following “opportunity” to sell a component product to a customer for $300. You can make the product for $100 in materials using 3 hours of labor but you need to use the constrained (bottleneck) resource to produce it. Or, you can outsource it for a mere $200. What should you do?

If using the bottleneck resource, you should “Buy it” because 3 hours of work on the constraint costs the organization approximately $750,100 of throughput ($6,000,000 / 24 hours = $250,000 / hr X 3 hours plus $100 of materials), not merely the $520 estimated by traditional cost accounting methods.

Again, if you have unused (non-pacesetter, extra, excess, protective) capacity already in-house, then use it to make things that will sell. The incremental cost will probably only be materials and the result in the case of a sale will be more revenue (contribution to overhead and profit) than the cost of those materials. In the case of an internal transfer, the result will be better utilization of your fixed assets and better return on total investment. (Incidentally, I hope you do have extra or protective capacity in-house, but that’s another article!)

To Summarize:

1. Assignments of most costs to time periods or events are arbitrary (even if in accordance with GAAP and IRS) and became relatively fixed at the time when you acquired the resource or asset (land, buildings, machinery, information systems, people’s services, etc.).

2. Know where your revenue flow bottleneck is.

3. Marginal cash flow cost at the non-bottleneck is usually only materials.

4. A transfer is not a sale (even if your software labels it as such) and does not generate real profit.

5. Using your non-bottleneck capacity to generate income from sales (not transfers) will generate cash flow and profits for you.

Hank Barr, CPIM-F is a past President and Director of Education for the Puget Sound, WA, USA chapter of APICS and a retired US Air Force Supply & Logistics officer. He is an active speaker and has taught Operations Management at several universities in the Pacific Northwest. Hank’'s certification clients include Tektronics, Boeing, Starbucks, Amazon, and Port of Seattle.